Please provide your information and submit this form. Our team will be in touch with you shortly.

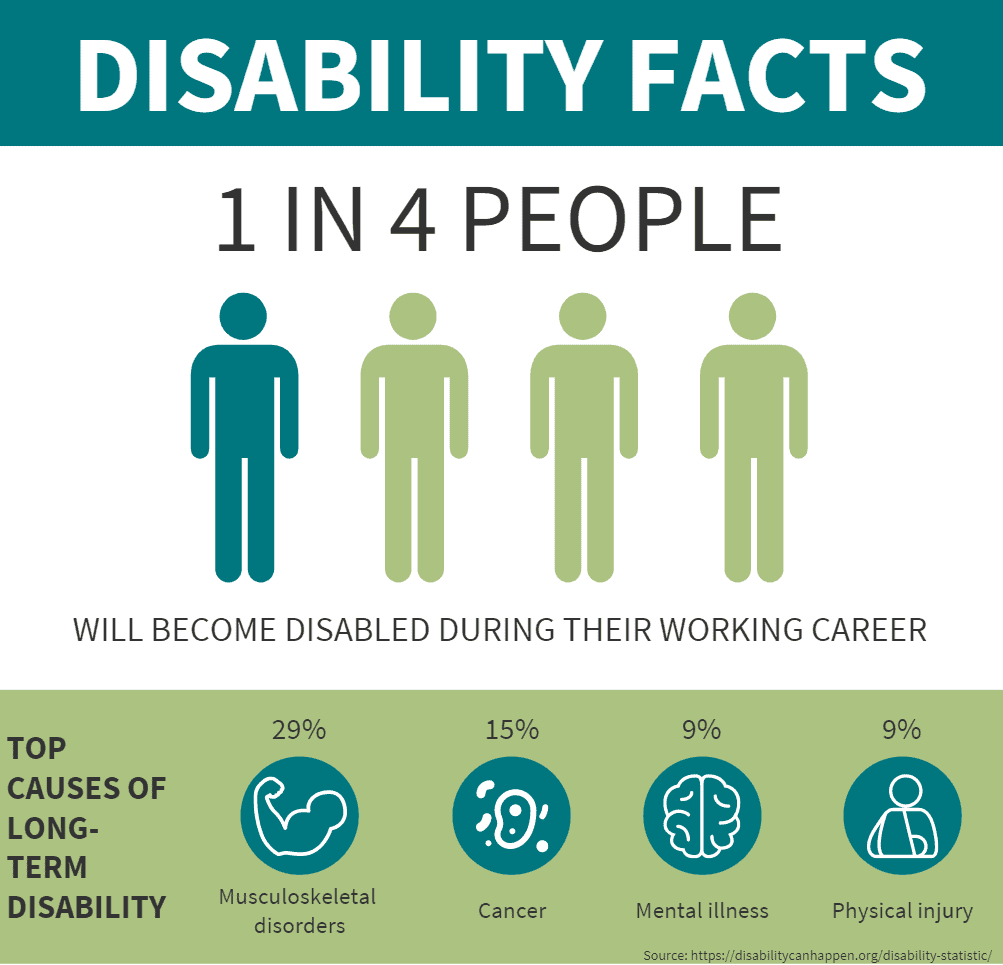

In our last series, we talked about the basics of life insurance, and depending on your financial situation, life insurance can be key to the success of your financial plan. Life insurance replaces your income for your dependents after you pass. But what if you need to replace your income while you’re still alive and disabled? Becoming disabled and not being able to work is more common than you’d think. In fact, it’s three to five times more likely to become disabled than to pass away prematurely, yet people are more financially prepared for their potential premature death than disability! If you are looking to learn about the basics and benefits of disability insurance, how much of it you need, and other ways to plan for disability, this series is a great starting point.

Definitions

The purpose of disability insurance is to replace your income for you and your dependents if you become disabled and can’t work. The word “disabled” can mean different things depending on the type of policy you get. The two most common definitions of disability include “own occupation” and “any occupation.”

An own occupation policy provides coverage if you are disabled and can’t perform the duties of your specific occupation, even if you are still physically and mentally able to work in another occupation. For example, surgeons are compensated not only because of their skill but because of their knowledge. An injury could take away their skill of performing surgery but leave them with the knowledge to teach, manage the surgery center, or consult. Typically, these alternative occupations pay less than performing surgeries. An own occupation policy protects against this because even though the surgeons can work in other knowledge-based positions, they will be covered for their inability to perform their specific duties of performing surgeries. This policy tends to be more expensive because the policy is more specific to your profession, thus more likely to be paid out by the insurance company.

In contrast, an any occupation policy provides coverage only if you cannot perform the duties of any occupation for which you are suited by education, experience and training. Let’s look at the previous example of being a surgeon. If you had an any occupation disability policy in that situation, you would not be covered because you are able to work in another position that requires your knowledge of the field. Any occupation policies tend to be less costly because the insurance company is less likely to have to pay out benefits since the policy is stricter on what’s covered.

Types

Another way that disability insurance policies can differ is whether it is a short-term or long-term policy, or in other words, how long the policy will provide benefits. Short-term disability policies provide a benefit to you for about three to six months. On the other hand, long-term disability policies provide a benefit to you that can last 2 years, 10 years, or even until retirement.

A key feature of disability insurance is the elimination period, which is the amount of time you must wait until the benefits start kicking in. Typically, elimination periods for short-term policies are shorter (less than 14 days) while long-term policies have longer waiting periods (30-720 days).

Premiums

The premiums of disability insurance policies may also differ. With a level premium, you pay a fixed amount for the life of the policy. With this premium structure, you are paying more of the insurance cost up-front. The other kind of premium offered is a graded premium. With this premium structure, the premium slowly increases with time, thus the up-front cost of the policy is lower than a level premium policy.

Everyone’s disability insurance needs are different, so feel free to reach out to us if you have any questions regarding how disability insurance could be a piece to your financial plan. This information is not intended to be a substitute for specific individualized advice, and we suggest you discuss your specific situation with a qualified financial advisor.

https://www.leveragerx.com/blog/level-vs-graded-disability-insurance-premiums/

https://www.affordableinsuranceprotection.com/disability_facts